EVERYONE NEEDS CYBER INSURANCE- INCLUDING YOU! THIS VIDEO EXPLAINS WHY.

Every business needs a written disaster plan. This plan must be unique to your business, your facility and your employees. The plan must address a variety of potential disasters such as but not limited to:

The plan should go beyond just the identification of the potential threats to a business. It should address, in detail, the response the business and employees will take should the situation occurs.

Your team needs input and participation from all levels of the organization from upper management to the facilities staff. One of the biggest mistake an organization can make is to have only management involved in the formulation of a disaster plan. A diversified employee team will do a better job in creating an effective disaster plan that actually works and will create better “buy in” throughout the organization.

Continually train your supervisors and employees. Success will depend on the readiness of your organization to response adequately to threats. Once training or “test runs” are completed, obtain feedback from employees and supervisor, find out what worked and what didn’t.

Developing a plan and putting on the shelf will not cut it. Your disaster plan is a living document. It needs to be constantly updated as your company’s operations change and as the threats change. Ten years ago, the thought of having “active shooter” training seemed excessive, now it should be required.

Ultimately, insurance is really just a funding mechanism for responding to disasters, whether it is a fire, tornado, violent act, a liability claim or a car accident. It all boils down to the question, who pays for the damages and the expenses that are incurred. Does the business pay for it or is the risk transferred to an insurance policy. It is important to note that a good insurance program can offer funding that helps pay for some elements of a disaster plan.

Sexual harassment allegations in Hollywood continue to drive the media headlines. However, this is not a new phenomenon. Sexual Harassment prevention is and should be a priority for any business, school or church.

We recommend 3 Steps in making sure your organization is taking steps to prevent sexual harassment from occurring in your work place.

Every business needs to have an anti-harassment statement. This statement is usually found in the Employee Manual or may be a separate form. It defines what sexual harassment is and gives information to employees on how to report such allegations and the steps the business will take to investigate the allegation. Most importantly, it states that sexual harassment will not be tolerated.

Supervisors are your front-line defense in preventing sexual abuse claims. Supervisors need to be trained regularly on how to identify potential problems and how to properly respond should an allegation be made. The response is crucial in these situations and if handled inappropriately can be costly to the business.

We recommend that every business has employment practices coverage. This coverage is either added to a package policy (you would see a separate limit for employment practices liability) or it will be a stand-alone policy.

Regardless, this coverage is not written on a standardized form, therefore each company’s version of this coverage could be different. It is extremely important to evaluate this coverage with an insurance professional to make sure your policy will respond to an allegation appropriately.

Preventing sexual harassment in the workplace requires a proactive mindset from management. Our agency can help your business, church or school maintain a strong anti-harassment environment.

Also, The Shropshire Agency has many tools that can help you regarding, but not limited to:

Call us today at 806.763.7311 so we can get started.

Unfortunately, we are continuing to see more and more high-profile cases of sexual harassment in today’s news. Many of these cases are drawing attention due to the harassment taking place in the entertainment and media industries as well as politicians.

As bad as many of these cases are, it is a reminder to all businesses and institutions of their responsibility to denounce sexual harassment in their workplaces, enforce the policies and procedures that are already in place when a situation happens, and to review those policies frequently with employees.

A report from the Equal Employment Opportunity Commission’s (EEOC) website highlight’s five core principles that have proven effective in stopping harassment from occurring in the workplace.

Being proactive is the most constructive approach for any business to prevent sexual harassment. Denying and ignoring this issue is not a good idea. Maybe now is a good time to review your current policies and procedures. If so, give us a call and we will be glad to assist your company.

If your company does not have an Employment Practices Liability Insurance (EPLI) policy, we can help get you coverage, if you do have an EPLI policy, let’s sit down and review the policy. EPLI policies are NOT standard policies, in that each one can cover or exclude different exposures.

Let’s start working together today, call us at 806.763.7311 to schedule an onsite consultation.

To view link to entire EEOC article- https://www.eeoc.gov/eeoc/publications/promising-practices.cfm

Check out our Business Insurance page to learn about important coverage for your Business.

Recently, The FBI published an article to help all for and not-for-profit businesses protect themselves against Ransomware attacks.

These attacks are occurring more frequently and they are no longer just directed towards the larger corporations. School, Churches and Small Businesses are receiving much attention from these criminals. The attacks are becoming more sophisticated and harder to prevent.

Ransomware attacks are resonated with a malicious email. A person will open an email, click an attachment, and that sets off a chain of events that are disastrous. The opened attachment releases an “infected program” that raids the computer’s data, encrypts it and makes it impossible for the owner to view their own data.

At the end of the process you will receive notification from the criminal that they now have possession of your data and if you want it back, you will have to pay for it.

Many experts say it’s not “if” you are going to be attacked, but “when.” So now is the perfect time to put measures in place on how to prevent an attack and how to respond should an attack occurs. These measures should include corporate policies and procedures regarding computer usage and emails along with computer hardware and firewall upgrades.

All businesses should consider purchasing a Cyber Liability policy. These policies are not standardized forms in that each policy can provide different types of coverage so it is vitally important to have an agent who understands the coverage and can help you choose the best policy for your company.

We can! The Shropshire Agency can provide your business with assessment tools to help you determine your level of risk of a Ransomware Attack. We can also help you establish internal controls to reduce the risk of ever having a claim. Finally, if you decide to pursue a Cyber Liability policy, we can help find the best policy for your company.

If you have any questions, don’t hesitate to call us at 806.763.7311

To read the entire article from the FBI, you can go to https://www.fbi.gov/investigate/cyber

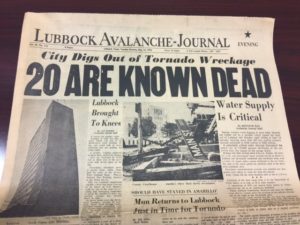

There is a difference between just talking about disasters and living through one.

On May 11, 1970, Lubbock Texas was struck by a large tornado. This tornado ravaged the downtown area and caused many deaths.

At that time, our agency’s address was 811 Ave M. and that was considered to be “ground zero” of the destruction. Only one wall remained of our agency, it was a total loss. Our CEO, Johnny Shropshire spent that night sitting on the rubble of agency to protect it from further damage and looters. He said the overwhelming smell of gas that the popping of electrical conduits continued for hours in the dark night.

The storm was extremely powerful. My grandfather had left a rather large insurance policy on his desk that evening. Four months later, a farmer in Floydada Texas (approximately 60 miles away) found it in his cotton field and mailed it back to us.

Our agency felt the impact of that night both as a business and a community member. We saw a community come together, help each other and rebuild.

We know what it like to almost lose everything but we also know what it is like to build it back. We also learned how to be prepared for the next one.

That experience etched in stone the purpose of our company and that is to protect families and businesses from the financial peril of a disaster.

Our agency insures many businesses of all sizes. When working with new clients, we are often surprised to find that many businesses are not fully educated about some very important coverage and risk management techniques that could be critical to their operation. So, based on our experience, we would like to share with you our 4 Insurance Gaps for Businesses that we consistently see in our reviews that could cost your business substantial monies.

Below are the areas where we find either:

Cyber Insurance– almost every business is dependent upon computer technology. Therefore, these businesses have exposures such as but not limited to: being hacked, passing along a computer virus to someone else, having one’s identity stolen, liability from having a website and all the notification expenses that are incurred should one of these events occur. There are no industry standardized forms so each policy can provide or leave out important coverage

Employment Practices Liability– provides coverage for allegations and claims involving sexual harassment, wrongful termination and discrimination. There are no industry standardized forms so each policy can provide or leave out important coverage

Property Coverage– property coverage seems simple, but over the years we have been amazed at how property values are evaluated and the types of forms being used to insure the Building and Business Property thus resulting in partial or no coverage.

Policies and Procedures– this is the proactive side of insurance. This includes such items as employee manuals, safety manuals and HR procedures to just name a few. Many businesses have them but fail to update them and use them as living documents in the business.

We all know that premium prices drive many of the buying decisions, but what if the lower premium doesn’t provide the coverage?

The Shropshire Agency will help you review your exposure to these and other threats to your business. Call us at 806.763.7311

Visit our Commercial Lines insurance page for more help for your company.

This is a question we ask all of our private school clients. The answer to this question will determine if a school can survive a disaster regardless of the insurance coverage.

Insurance is a financial component to help protect a school. It is important that the insurance addresses the liability exposures of the school, the school’s property and the loss of income and extra expenses that could occur after the incident.

Be careful, many times we find schools missing significant coverages that could impact the school greatly.

Along with having good insurance coverage, it is just as important to have a detailed plan to help you react effectively to a disaster.

You receive a call at 2:30 am that your school is engulfed in flames. By the time you arrive at the school it is obvious that there is significant damage and the school will be uninhabitable for some time. Do you have a plan?

These are just a few questions that would need to be addressed but they are just the tip of the iceburg.

Fires and tornadoes are disasters that schools typically address; however, we generally find that the plans do not go deep enough with the goal being to maintain and even grow the current level of students, even if you not residing in the school building for up to 18 months.

Disaster plans need to address the obvious and the unthinkable situations such as but not limited to a flood, utility outages or leaks, “active shooter situations,” automobile accidents, death of a student or administrator, threats made to the school, influenza and other communicable diseases, sexual misconduct allegation or any other criminal acts. This plan should also include a financial contingency plan for the situations such as loss of a significant donor or grant funding.

The goal of a Disaster Plan is to keep your school in business and thriving after an unfortunate event.

We would be glad to meet with you and discuss our services and resources to see if we can help your school in any way.

Contact us at 806.763.7311 or complete our contact form.

Check out our Commercial Insurance Services and Product by clicking here.